Shawarma Capital Portfolio Update - June 15, 2026

2 months in… up 50%

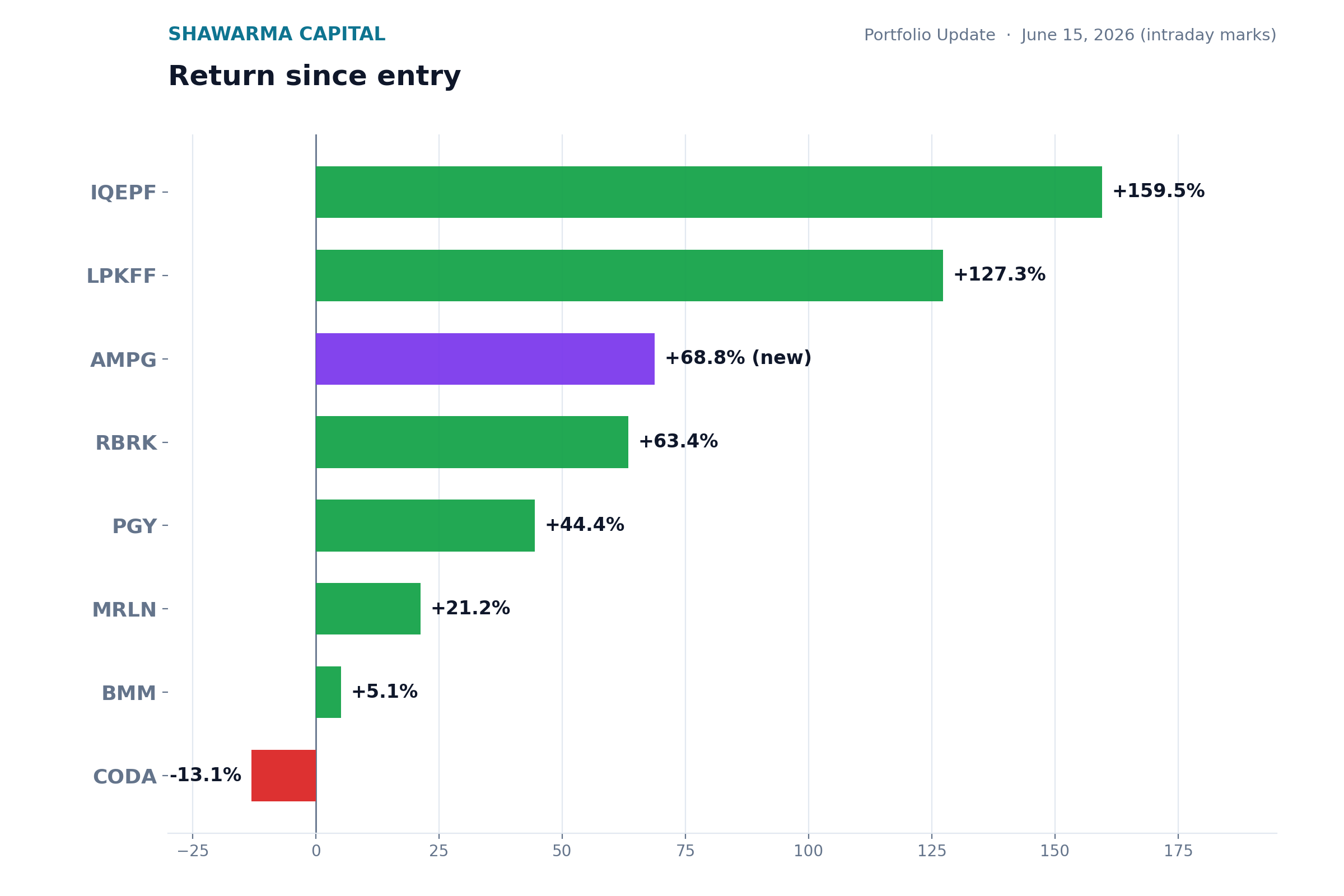

MRLN +21.2% - The C-130J critical design review cleared with USSOCOM on June 4 and moved the program from design into aircraft integration on the hundred-million-plus IDIQ ceiling. Management restated the plan to fly a crewed fixed-wing aircraft autonomously in commercial revenue service from New Zealand in 2027, gated on finishing certification by year end. I shipped Part 10, Part 11, and a live OSINT tool that tracks every Merlin tail by FAA owner record. The tape gave back the design-review pop and trades near $7.31, up about a fifth from the October entry. None of the seven kill criteria have been met.

IQEPF +159.5% - IQE signed a multi-year indium phosphide epiwafer supply agreement with Tower Semiconductor for AI data-center optical connectivity, with first-year minimum purchase commitments, and settled the prior IP dispute in the same stroke. An £81M raise earlier cleared the bank debt and the company guides to more than 20 percent revenue growth this year. The stock is up double digits intraday on the Tower print. Position grew through price action, no fresh capital added.

LPKFF +127.3% - The activist standoff went to a vote at the June 4 annual meeting and management won. LPK.DE popped to €23.60 on the result and settled near €21.50. The glass-substrate AI packaging monopoly thesis is intact and Part 4 is live. Plan is still to size back in on dips once BMM re-rates.

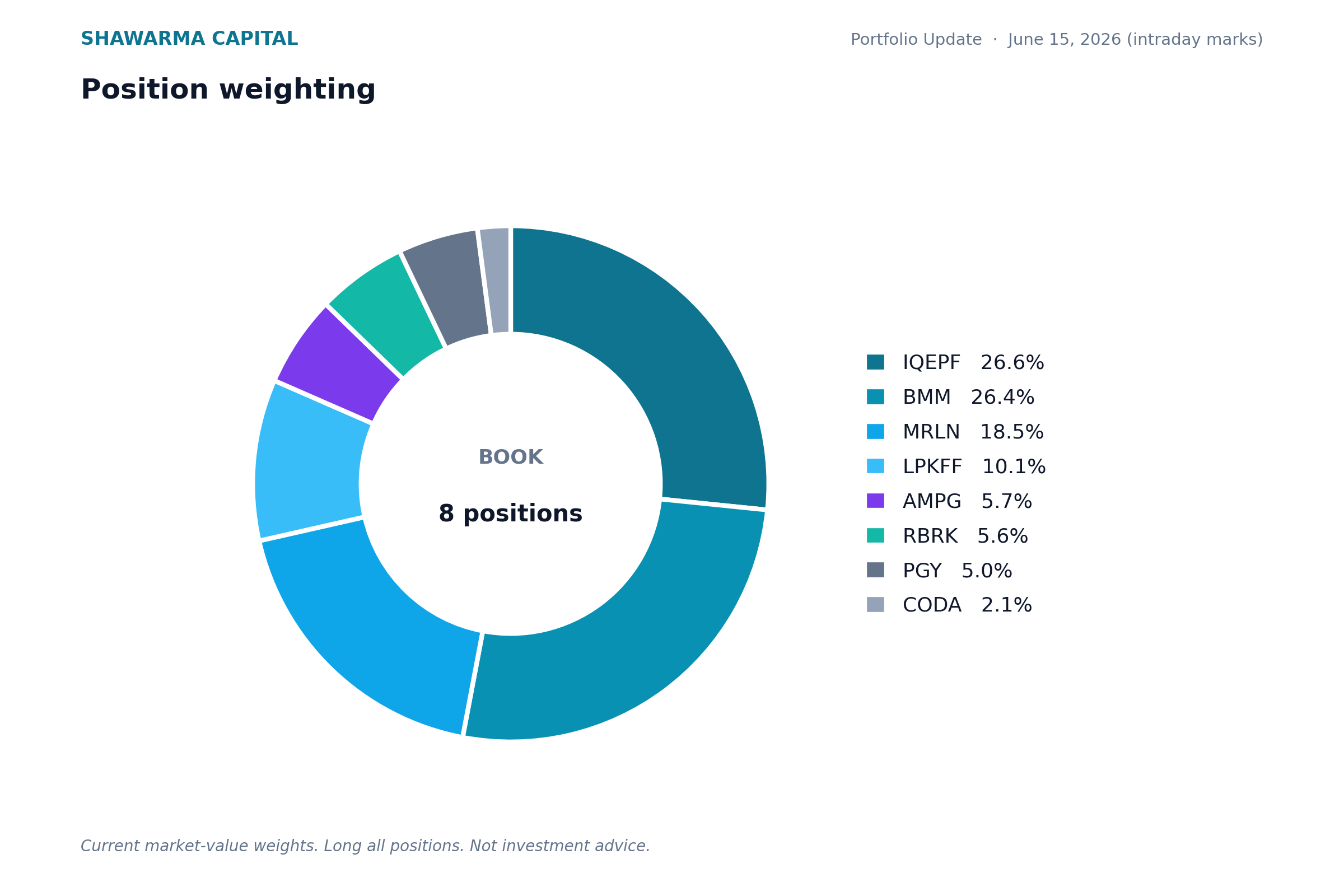

BMM +5.1% - Blue Moon Metals consolidated after Part 3. Springer in Nevada is still the only permitted US-domiciled ammonium paratungstate hub, and Nussir in Norway carries the EU Critical Raw Materials Act strategic designation after closing its C$156.3M bought deal. Building toward the 35 percent target weight, the largest position in the book. The probability-weighted expected value against today's print keeps the asymmetry wide.

AMPG +68.8% - New starter taken in early June at $4.50, about five percent of the book. AmpliTech is a twenty-four-year-old RF house that turned itself into a 5G open-RAN radio OEM with a quantum tail, printing 48 percent gross margins with no debt. The first conversion landed on the record this month: FCC and ISED cleared the radio and the BEAD program money started to move. It already trades near $7.59, through the seven-dollar target I underwrote it against. The asymmetry on a five-dollar microcap is wider than anything else I own.

RBRK +63.4% - Rubrik beat every metric in the Q1 fiscal 2027 print on June 4 and raised full-year guidance across the board. Subscription ARR grew 32 percent to $1.57B, revenue grew 39 percent, and the subscription contribution margin widened to 13.2 percent from 8 percent a year ago. Thesis intact, no exit, the light haircut to fund the BMM build stays.

PGY +44.4% - Pagaya posted its first clean GAAP profit in Q1, $25M of net income against a loss a year ago, on $318M of revenue and $2.6B of network volume, and raised the 2026 guide. A CFO transition takes effect mid-June. Quiet execution, no drama, the tape finally repriced it.

CODA -13.1% - Coda Octopus gave back the year's gain into the microcap pullback and now sits below my basis. Underwater imaging for defense and offshore energy, still profitable and debt-free. Thesis intact, plan is to size back in on dips post-BMM re-rate.

See you mid-July.

Long all positions. Not investment advice.

Looks good. Thoughts on coda quarter ? Market selling off results.

Where is bGDE?