Shawarma Capital Portfolio Update - May 14, 2026

Seven weeks in. Seven for Seven.

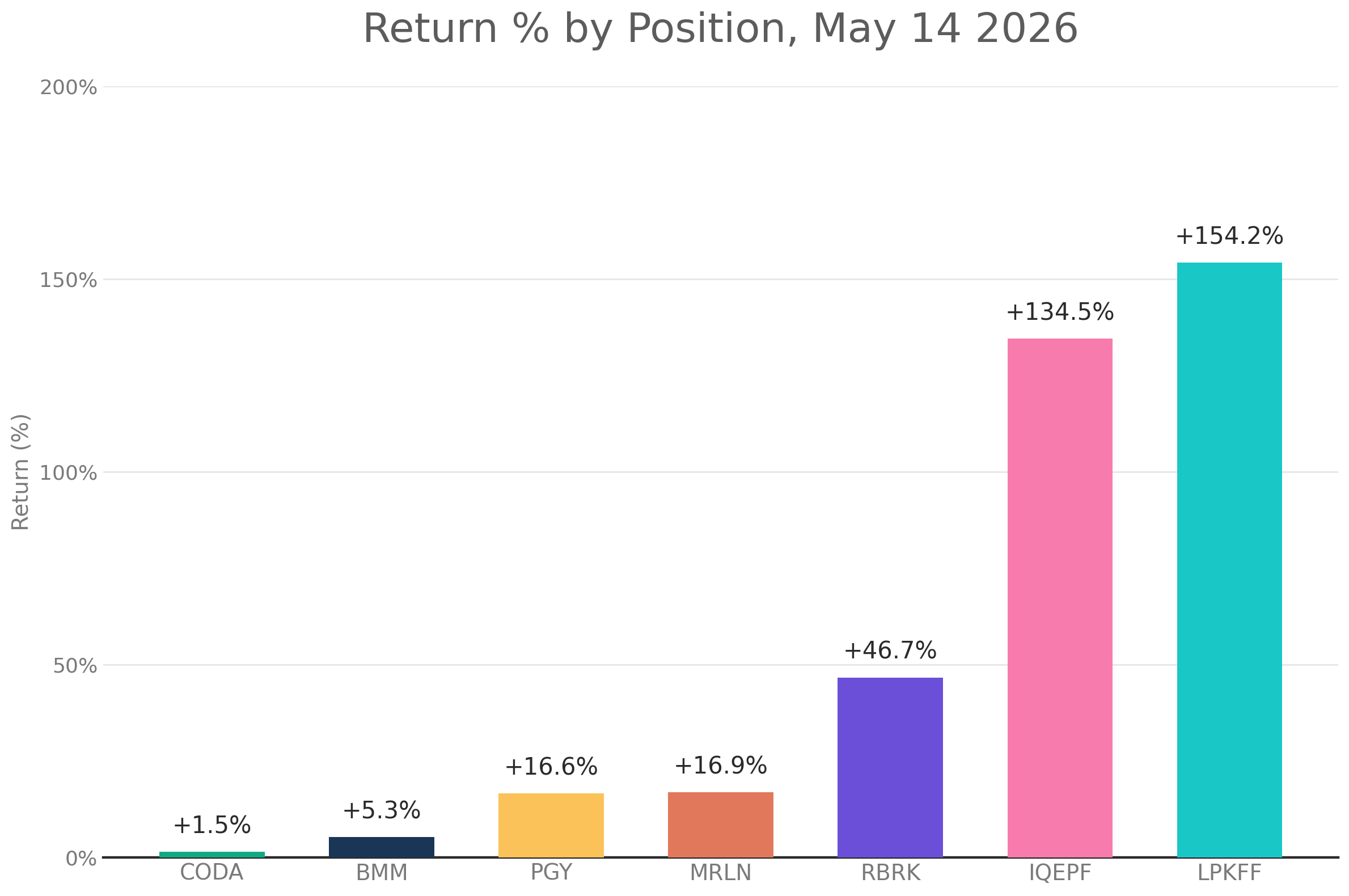

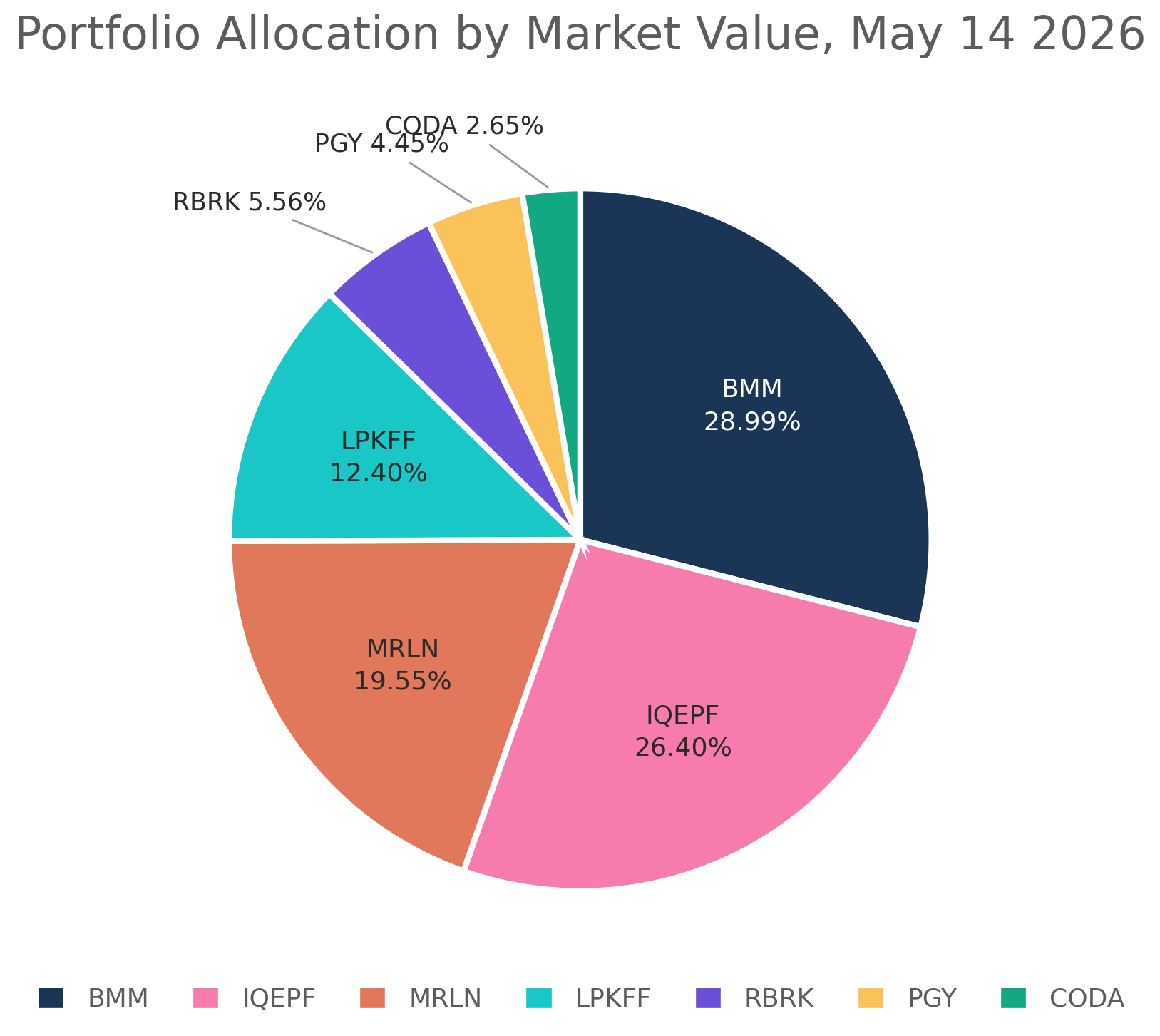

MRLN +16.9% - Q1 dropped this morning. Revenue $1.0M, Adjusted EBITDA loss $23.3M, headline GAAP net loss of $90.4M was 96% non-cash mark-to-market on convertible promissory notes from the de-SPAC. Cash position post-PIPE is approximately $183M with no debt. CFO Carrithers said the runway extends beyond the near-term certification and commercial milestones. CEO Matt George revealed Condor, the first product family, paired with a non-binding MOU with World Star Aviation for commercial cargo. The tape sold 10.5% on the resale registration becoming effective. None of the seven kill criteria have been met. Full Part 8 is live.

LPKFF +154.2% - LPKF Laser ran from the April 16 mark of $13.30 to the May 14 mark of $27.96. Glass-substrate AI packaging exposure, exclusive CPO partnership. Management Q1 framing explicitly invited measurement against production order wins this year. Plan is to size back in on dips once BMM re-rates.

IQEPF +134.5% - IQE compound semiconductor wafers. MACOM closed the £45M acquisition of the Welsh fabs and signed a ten-year supply agreement to buy product from the same fabs they now own. Customer-becomes-owner structure on the deal compresses the re-rate path. Position grew through price action, no fresh capital added.

RBRK +46.7% - Rubrik flipped FCF from $24M to $238M year over year at $1.5B ARR. Tape ran the position past prior gains into the broader software re-rate. Thesis intact, no exit, light haircut to fund the BMM build.

PGY +16.6% - Pagaya AI credit platform. Quiet execution continues. Tape priced through the broader AI-credit cohort move without drama.

BMM +5.3% - New position since the prior update. Building toward the 35 percent target weight, currently the third-largest position behind IQE and MRLN by allocation. Springer in Nevada is the only permitted US-domiciled ammonium paratungstate hub. Nussir in Norway closed the C$156.3M bought deal on May 6 and holds an EU Critical Raw Materials Act Strategic Project designation. Probability-weighted expected value of $59.90 against today's $7.16 print is an 8.3x.

CODA +1.5% - Coda Octopus underwater imaging for defense and offshore energy. Profitable, debt-free. Tape gave back most of the April gain into the broader microcap pullback. Thesis intact, plan is to size back in on dips post-BMM re-rate.

See you mid-June.

Long all positions. Not investment advice.

No AMPX?