Shawarma Capital Portfolio Update: July 11, 2026

3.5 months in.

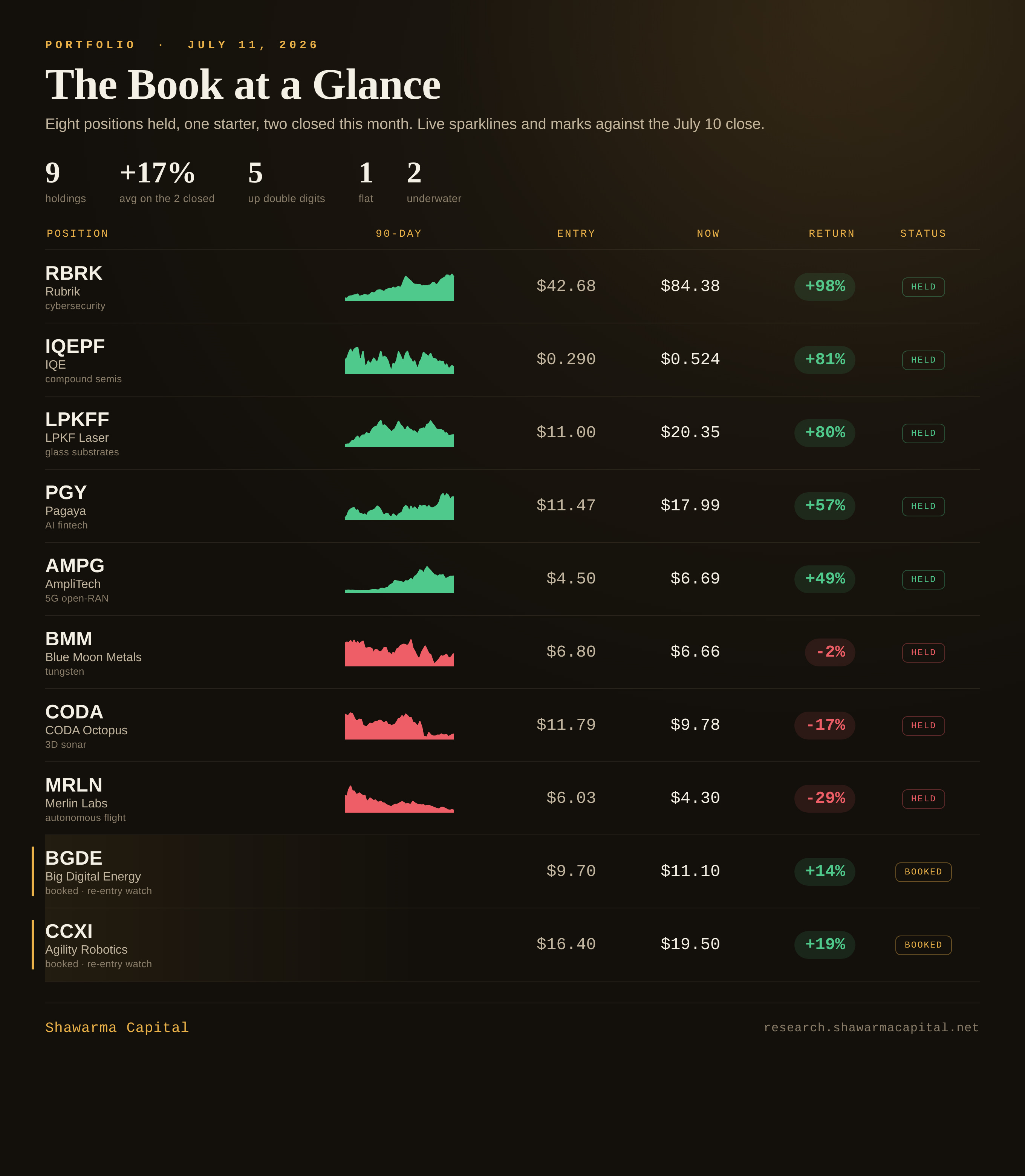

The book did two things this month. It booked two fast round-trips, and it took a drawdown on the flagship that I am going to walk through in full rather than bury. Everything below is marked against the July 10 close. New here? Start with Who Is Shawarma Capital, then come back.

Two round-trips, booked

I closed two positions this month, both for the same reason. I bought a fast setup, the re-rate came, and I would rather bank the gain and step aside than sit through the near-term volatility these two names carry. Both fluctuate hard, several dollars in a session. Both are still on my coverage list, and I am assessing re-entry on each once the short-term chop settles. This was a volatility decision, not a thesis exit.

BGDE, +14 percent. I bought Big Digital Energy at the first-post level on June 17, the evening the 129-megawatt writeup went out, and sold at $11.10 into the re-rate a week later. A failed bitcoin miner sitting on scarce, grid-connected PJM power, an insider group buying on the open market from four dollars to over eight, and a shell repricing from sixteen to forty million dollars. The trade was the re-rate, and it came fast, from the mid-eights through eleven and change and straight back down. That swing is exactly what I stepped aside from. I still cover the name and shipped a Part 2 on the financing tell. I am watching for a cleaner re-entry.

CCXI, +19 percent. I bought Agility Robotics through the CCXI trust at $16.40 on June 29, as it finally broke off the ten-dollar floor, and sold at $19.50 into the spike two sessions later. The liquid, pre-close way to own the only humanoid that already moves totes for paying customers. The stock ran from ten to nearly twenty in two weeks and gives back three and four dollars in a day. I booked the move and I am letting the volatility cool before I decide on re-entry.

The held book, by return

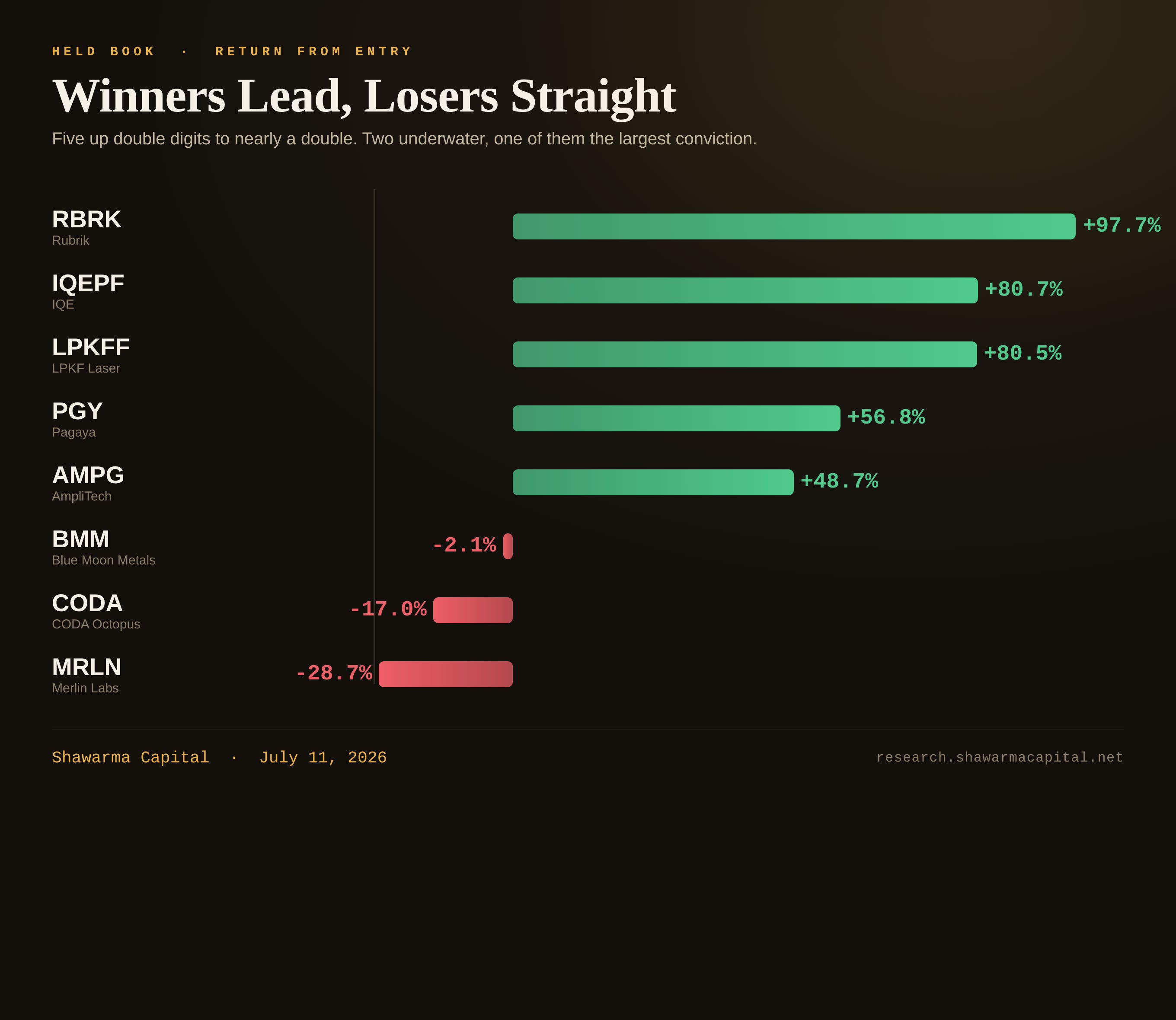

The held book splits clean. Five winners, from a Rubrik near a double down to AmpliTech at plus forty-nine, one position flat, one starter I am still adding to, and two underwater, one of them my largest single-name conviction.

RBRK, +98 percent. Rubrik nearly doubled from my basis. The Q1 fiscal 2027 print beat every metric and raised guidance across the board, subscription ARR up 32 percent to $1.57B, revenue up 39 percent, and the subscription contribution margin widened to 13.2 percent from 8 percent a year ago. The AI control plane thesis is playing out in the numbers, not the narrative. No exit. The small haircut that funded the BMM build stays.

IQEPF, +81 percent. IQE signed the multi-year indium phosphide epiwafer supply agreement with Tower Semiconductor for AI data-center optics, with first-year minimum purchase commitments, and settled the old IP dispute in the same stroke. An earlier raise cleared the bank debt, and the company guides to more than 20 percent revenue growth this year. The stock spiked on the Tower print and gave some back into the semis pullback. Position grew through price action, no fresh capital added.

LPKFF, +80 percent. The activist standoff went to a vote on June 4 and management won. The German listing gave back part of the pop into the broad small-cap pullback and trades near seventeen and a half euros, still a double from my basis. The glass-substrate AI packaging monopoly thesis is intact and Part 4 is live. The plan is still to size back in on dips once BMM re-rates.

PGY, +57 percent. Pagaya posted its first clean GAAP profit in Q1, twenty-five million of net income on $318M of revenue and $2.6B of network volume, and raised the 2026 guide. A CFO transition took effect mid-June. Quiet execution, and the tape finally repriced it. No change.

AMPG, +49 percent. AmpliTech ran through the seven-dollar target I underwrote it against and pulled back to the high sixes with the microcaps. The first conversion is on the record, FCC and ISED cleared the radio, and the BEAD program money is moving. A twenty-four-year-old RF house turned 5G open-RAN radio OEM with a quantum tail, printing 48 percent gross margins with no debt. Still the widest asymmetry on a five-dollar cost basis in the book. Held.

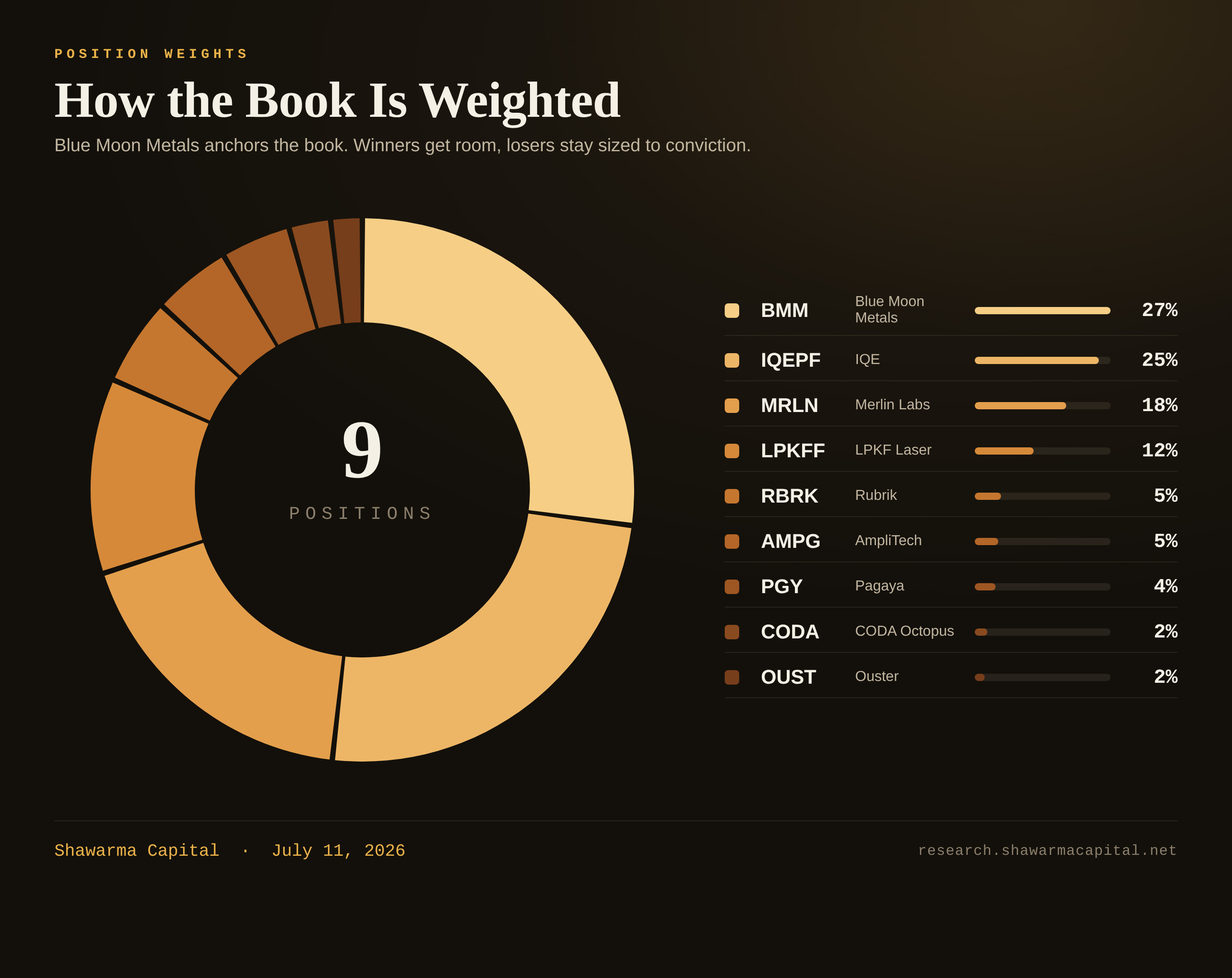

BMM, flat. Blue Moon Metals sits right on my basis after the consolidation. Springer in Nevada is still the only permitted US-domiciled ammonium paratungstate hub, and Nussir in Norway carries the EU Critical Raw Materials strategic designation after closing its C$156.3M bought deal. It is the largest position in the book, roughly a quarter of it, and I am still building toward the target weight. The probability-weighted expected value against a six-and-a-half-dollar print keeps the asymmetry wide.

OUST, starter. The lidar starter I opened in June is the one new name I am adding to rather than trimming. The Pentagon widened the China lidar ban to the top two suppliers, the Rev8 factory qualified for federal infrastructure dollars under Build America Buy America, and the company raised two hundred million into strength. It trades in the low forties. Small position, thesis compounding, and I am sizing it up on pullbacks.

CODA, -17 percent. Coda Octopus is still below my basis after the microcap drawdown. Real-time 3D sonar for defense and offshore energy, profitable and debt-free, with defense primes including Anduril moving into the channel. Thesis intact, and the plan is to size back in on dips.

MRLN, -29 percent. The one I owe you the straight version on. Merlin is my largest single-name conviction and it trades near a fifty-two-week low around four dollars and thirty cents, below my $6.03 basis. The move is supply, not story. The PIPE resale registrations went effective and pushed stock into a thin float, and the tape did what a thin float does. The operating case did not break. The C-130J critical design review cleared with USSOCOM, the program moved into aircraft integration on the hundred-million-plus IDIQ ceiling, the defense budget the thesis points at keeps inflecting, and none of the seven kill criteria have been met. I have not sold a share, and I built Merlin World so you can walk the fleet yourself. I am treating the supply as a gift, not a verdict.

How the book is weighted

Blue Moon Metals is the anchor, with IQE beside it and Merlin third. The winners get room, the losers stay sized to the conviction, and the cash the two round-trips freed up is dry powder for the re-entries and the BMM build.

What I am watching into August

MRLN, the next SOCOM C-130J task order window and the Q2 print with backlog, the first hard read on whether the loss narrows on plan.

OUST, Q2 earnings on August 6, the first look at the balance sheet after the two-hundred-million raise.

BGDE and CCXI, both on re-entry watch once the near-term volatility settles.

BMM, continued build toward the target weight as the Springer and Nussir permitting and financing steps land.

The full theses

Every position, in one place:

See you at the end of the month.

Long all held positions. The two trades above are closed and under re-entry review. Not investment advice.

Really appreciate the details

You do good work, and I really appreciate your thorough analysis of these companies. I already had owned $MRLN and since I found you guys on Substack, I have since bought $AMPG and $TRT. I looking into becoming a member at some point, thank you!